Abercrombie & Fitch Co (NYSE: ANF) Oversold, Tariff Fears, but a great opportunity?!

If you aren't scared of a little risk, and believe in the American economy, ANF could be a golden opportunity.

Quick Due Diligence Report: Abercrombie & Fitch Co. (ANF)

Company Overview

If you saw the photo and then clicked the link to bring you here, thats one reason you should at some point develop an intrance into A&F stock, these people can market. Abercrombie & Fitch Co. (NYSE: ANF) is a global specialty retailer offering casual apparel, personal care products, and accessories under brands including Abercrombie & Fitch, Abercrombie kids, Hollister, and Gilly Hicks. Headquartered in New Albany, Ohio, ANF operates across North America, Europe, the Middle East, and Asia-Pacific. The company has revitalized its brands through digital innovation and an omnichannel strategy, driving significant growth in recent years.

Financial Snapshot

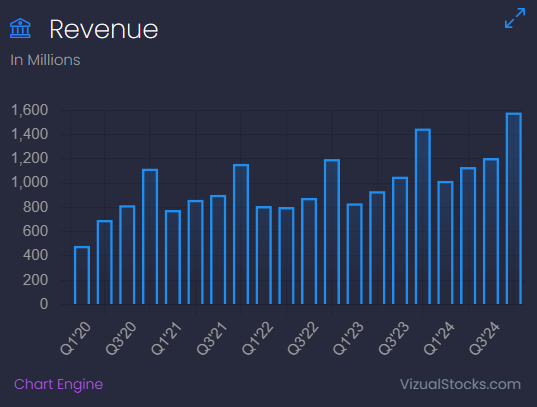

Revenue (Fiscal Year Ending Feb 3, 2024): $4.28 billion, up 15.76% from $3.70 billion in 2023.

Net Income: $566 million (up 72%)

Free Cash Flow: $527 million (up about 30%)

Debt to Equoty ratio: 0.70

Shares Outstanding: 50.37 million.

Market Capitalization: $4.33 billion (at $86.03 per share).

Stock Price Performance and Tariff Impact

Since the Jan 2025 tariff announcements, ANF’s stock has faced significant pressure. On March 5, 2025, ANF reported Q4 and full-year 2024 results, exceeding earnings estimates but issuing cautious 2025 guidance due to tariff-related costs. Market reports indicate a 15% drop that day, driven by holiday sales not meeting expectations and margin pressure forecasts of up to 100 basis points.

Pre-Tariff Peak (May 2024): $196.99.

Post-Tariff Decline: From $160.92 to $86.03 by March 8, 2025, reflecting major tariff fears and broader retail sector concerns.

Tariff Effect: ANF’s reliance on international sourcing exposes it to higher costs, threatening its gross margin (around 65%).

Discounted Cash Flow (DCF) Analysis

The DCF model estimates ANF’s intrinsic value by projecting free cash flows and discounting them to present value.

Assumptions

Revenue Growth Rate:

2025: 7% (down from 19.59% TTM due to tariff headwinds).

2026-2029: 6% average (recovery as tariffs potentially ease).

Terminal Growth Rate: 2% (long-term GDP growth proxy).

Operating Margin:

2025: 12% (down from ~14% TTM due to tariffs).

2026-2029: 13.5% (gradual recovery).

Terminal: 13%.

FCF Margin: ~9.5% of revenue (TTM basis), assumed to stabilize at 9%.

Projection Period: 5 years (2025-2029).

DCF Calculation

Intrinsic Value per Share:

7,923 / 50.5 = ~$157 per share.

DCF Result

At $157 per share, ANF appears undervalued relative to its current price of $86.03, suggesting a ~82% upside potential should the full weight of tariff fears not be realized and there is a recovery.

Internal Rate of Return (IRR) Analysis

Assuming a purchase at $86.03 today and holding until 2029, with a sale at the terminal value:

Initial Investment: -$86.03 per share.

Annual FCF per Share: $9.19 (2025), $9.74 (2026), $10.33 (2027), $10.95 (2028), $11.60 (2029).

Terminal Value per Share (2029): $182 (9,204 / 50.5).

Using an IRR calculator:

IRR ≈ 20.5%.

This exceeds the WACC (8.5%), indicating a strong return potential.

Tariff Impact and Rebound Potential

Current Impact: The drastic decline from the Janurary high of $160.92 to $86.03 reflects tariff-related fears, with a notable 15% drop on March 5, 2025, after Q4 results and guidance. Tariffs could reduce 2025 margins by 100 bps, impacting profitability.

Rebound Scenario: If tariffs are lifted by 2026 (e.g., due to policy reversal), ANF could see:

Revenue growth of 10-12% annually as costs normalize and consumer demand strengthens.

Operating margins recovering to 14-15%, lifting FCF to $550-600M annually.

Stock price potential: $170-$190 (P/E of 15x projected 2026 earnings of $11.33-$12.67 per share), a 98-121% increase from $86.03.

My Estimated Likelihood: Moderate, depending on trade policy shifts. ANF’s brand strength and operational resilience support a robust recovery, and they will certainly be able to weather the storm with their low debt.

Risks

Extended tariff enforcement could deepen margin erosion.

Economic slowdown reducing discretionary spending.

Conclusion

At $86.03, ANF is significantly undervalued per the DCF ($157), offering an 82% upside and a 20.5% IRR over five years. The stock has suffered a ~53% drop since tariff announcements, but its fundamentals remain solid. A tariff removal could drive a rebound to $170-$190 by 2026-2027, leveraging ANF’s strong brand and omnichannel capabilities. Investors should weigh tariff policy developments against this opportunity.

Another interesting pitch, US retailer, P/E and P/FCF are around 8x. Regarding the tariffs, only around 35% goes to the cost of the goods, and 80% of revenue from US, so total effect would be 28% times new tariffs. Plus, are any clothing company that doesn't outsource production abroad, so competitors need to increase prices too. Plus it is easy to move these kind of production to other countries, this is not high tech, the value is the branding and distribution.