I will NEVER pay ANY tax on my trading and investing accounts, ask me how!

How putting a tax-free wrapper on my trading account bought me a Cadillac in retirement!

Pardon my clickbait, I’m experimenting here.

TLDR: I have as much of my money in Roth IRAs for investment purposes as possible. You can trade stocks, ETFs, options, doing almost anything a standard investor would want to do, all tax-free. If you want a few more details, read the rest.

So, I woke up one rainy day when I couldn’t work and looked at my bank account. I had a decent chunk of change, a new deposit I'd already paid taxes on. I started thinking about investing it and doing some math on what it would look like to have money to retire with someday. If it grew like it was supposed to, I'd end up with way more than five times what I started without ever investing anything more than the original deposit! But then I realized that when I took that money out of my Robinhood account, I'd have to pay capital gains taxes on all the money that I grew that money into. Those taxes would be even more than my total original deposit!

That got me thinking about how to not pay taxes twice. I was pretty strapped for cash at the time, basically living on ramen, but I started digging into ways to protect my money. That's when I found out about Roth IRAs. Since I'd already paid taxes on the money, and it was prior to that year’s tax day, I could put in $14,000, covering both the past year and the current year. I basically used up all my cash, but then I started investing in stocks, knowing any gains I made would be tax-free when I retired. It felt like I'd found a way to outsmart the system.

Trading stocks inside a Roth IRA offers several financial benefits for the average Cody like me, primarily centered around tax advantages and flexibility for long-term wealth building which checked every single one of my boxes. Here’s a detailed breakdown of the key benefits:

1. Tax-Free Growth

How it Works: 100% of your profits from trading stocks (capital gains, dividends, or interest) within a Roth IRA grow tax-free. Unlike a taxable brokerage account, where you’d owe taxes on realized gains each year, a Roth IRA shields all investment earnings from taxation.

Benefit: This allows your money to compound more effectively over time. For example, if you buy a stock for $1,000 and sell it later for $5,000, that $4,000 gain is entirely yours—no capital gains tax applies, whether short-term (higher rates) or long-term.

2. Tax-Free Withdrawals in Retirement

How it Works: Since contributions to a Roth IRA are made with after-tax dollars, qualified withdrawals (typically after age 59½ and if the account has been open for at least 5 years) are completely tax-free, including all gains from stock trading.

Benefit: This is a huge advantage compared to a traditional IRA or taxable account, where withdrawals are taxed as income or gains are taxed upon sale. You can trade aggressively or conservatively within the Roth IRA and enjoy the full proceeds later without a tax hit.

3. No Required Minimum Distributions (RMDs)

How it Works: Unlike a traditional IRA, which mandates withdrawals starting at age 73, a Roth IRA has no RMDs during your lifetime.

Benefit: You can keep trading stocks and growing your account indefinitely, letting your investments compound without being forced to sell or withdraw. This flexibility is ideal for active traders who want to maintain control over their portfolios and pass wealth to heirs.

4. Flexibility in Trading Strategy

How it Works: Since gains are tax-free, you can trade stocks more frequently (e.g., day trading or swing trading) without worrying about short-term capital gains taxes, which are taxed at higher ordinary income rates in a taxable account.

Benefit: This encourages a more dynamic approach to stock trading. For instance, you can capitalize on short-term market movements without the tax penalty that might deter such strategies outside a Roth IRA.

5. Protection from Future Tax Rate Increases

How it Works: By paying taxes on contributions upfront (at your current tax rate), you lock in tax-free growth and withdrawals regardless of future tax policy changes.

Benefit: If tax rates rise in the future—say, due to government policy shifts—you’re insulated from higher capital gains or income taxes on your stock trading profits, making the Roth IRA a hedge against uncertainty.

6. Diversification and Risk Management

How it Works: A Roth IRA allows you to trade a wide range of stocks (and other assets like ETFs or mutual funds), giving you the ability to diversify your portfolio within a tax-advantaged wrapper.

Benefit: You can balance high-risk, high-reward trades with more stable investments, knowing that all gains are tax-free, which might make you more comfortable taking calculated risks.

7. Contribution Withdrawals Anytime

How it Works: You can withdraw your Roth IRA contributions (not earnings) at any time, tax and penalty-free, regardless of age or holding period.

Benefit: This provides liquidity and peace of mind. If you need to access the money you put in (not the gains from trading), you’re not locked in, though earnings must stay until retirement to avoid taxes and penalties.

Practical Example:

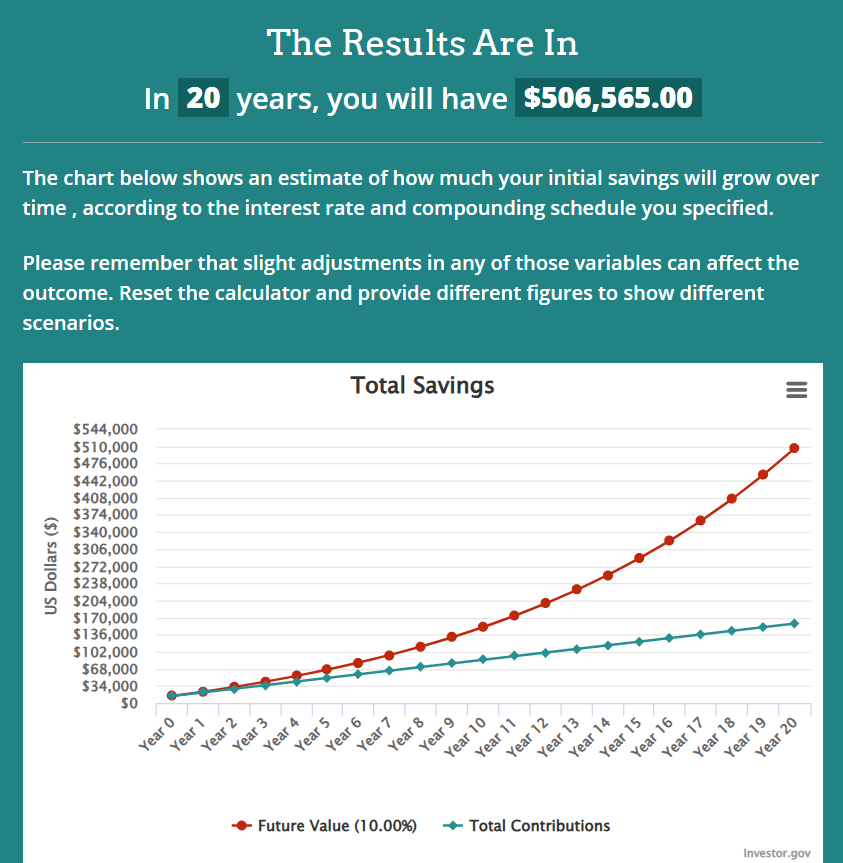

Imagine you contribute $14,000 (the 2025 annual limit for those under 50 who haven’t contributed in 2024 yet) to a Roth IRA and use it to trade stocks, you also contribute your annual maximum. Over 20 years, through smart trading, it grows to $506,565 (10% annually) on a total contribution of about $160,000. In a taxable account, you might owe 15% long-term capital gains tax on the $348,565 profit ($52,284), reducing your take-home to just over $450,000 (still a large amount of money, but a paid-in cash brand-new car short of what you could have had). In a Roth IRA, you keep the full $506,565, tax-free, assuming you are 59.5 years old at the time and can buy that Cadillac guilt-free on Uncle Sam’s dime.

Limitations to Consider:

Contribution Limits: In 2025, you can only contribute $7,000 annually ($8,000 if 50 or older), limiting how much you can trade with compared to a taxable account.

Early Withdrawal Penalties: If you withdraw earnings (not contributions) before age 59½ and the 5-year rule, you’ll face a 10% penalty plus taxes on those gains.

No Tax Loss Harvesting: In a taxable account, you can offset gains with losses for tax purposes; this isn’t an option in a Roth IRA since taxes don’t apply.

Who Benefits Most?

Young Investors: With decades for compounding, even small stock-trading gains can grow significantly tax-free.

Active Traders: Frequent trading without tax consequences maximizes profits.

High Earners Expecting Higher Future Taxes: Prepaying taxes now at a lower rate secures tax-free gains later.