Managing Risk in the market landscape of 2025

60/40 vs Other Portfolio Options

When I was on active duty in the Marine Corps I worked in the Yuma Air Traffic Control tower, as a Tower Controller. Risk was something that we had been tirelessly trained to be averse to, however even in that environment, the risk was something we managed so we could accomplish what we wanted to accomplish. We were constantly weighing a cost-benefit analysis of how much risk we could accept in any given situation to get planes either off of or onto the tarmac as expeditiously as possible while maintaining an acceptable level of safety.

But let’s be real, we are talking about the US stock market, and putting your hard-earned dollar in the stock market always comes with an element of risk. So as we are starting to move through 2025, there are strategic ways to manage and potentially mitigate those risks amid a confusing political and economic landscape that is hard to predict day to day. Understanding your personal risk tolerance, investment goals, and the economic context is crucial, if you love risk please feel free to stop reading right here. The aim of investing for me and my clients is not just to protect our capital but also to position our portfolios for growth in various market conditions. Here are several considerations I have for managing investment risk in the coming year.

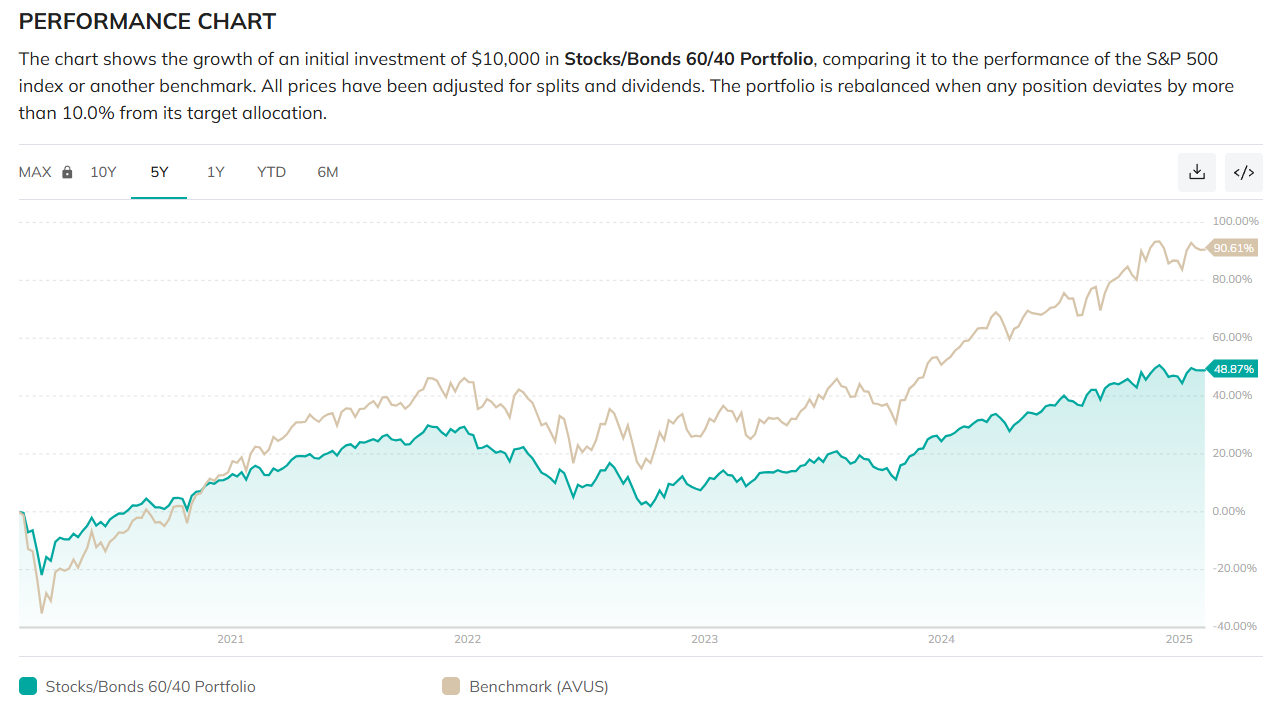

An old-fashioned approach to risk management is the 60/40 portfolio, where 60% of your investments are in equities and 40% in bonds, this will never give you the best returns available on the year, but also it’s just boring. I have heard it said that you are at the appropriate level of risk management if you hate part of your portfolio, but I also don’t think that is necessary. Yet this model has historically provided a balance that can cushion investors against market volatility while sacrificing a significant portion of potential gains. However, in 2025, the bond portion might not provide the same level of safety or return as in the past. This could lead to a scenario where your bonds are less effective at offsetting stock market downturns, exposing you to what might be termed "unscary" risk - not catastrophic, but still noticeable. You can see by the graph below the benchmark 60/40 portfolio had very similar drops over the last 5 years as the Equities diverse SP500 Equities Portfolio.

In the pursuit of achieving all-weather performance, diversification beyond the simple stock-bond split is essential. This involves spreading your investments across various asset classes, sectors, and even geographic regions. Consider adding commodities, real estate, or even alternative investments like private equity or hedge funds. The idea is to have assets that perform differently under different economic conditions - some might thrive in inflation, others in deflation, some during growth, others in recession. This broad diversification can help your portfolio navigate through diverse economic landscapes, potentially reducing the impact of any single market downturn on your overall investment.

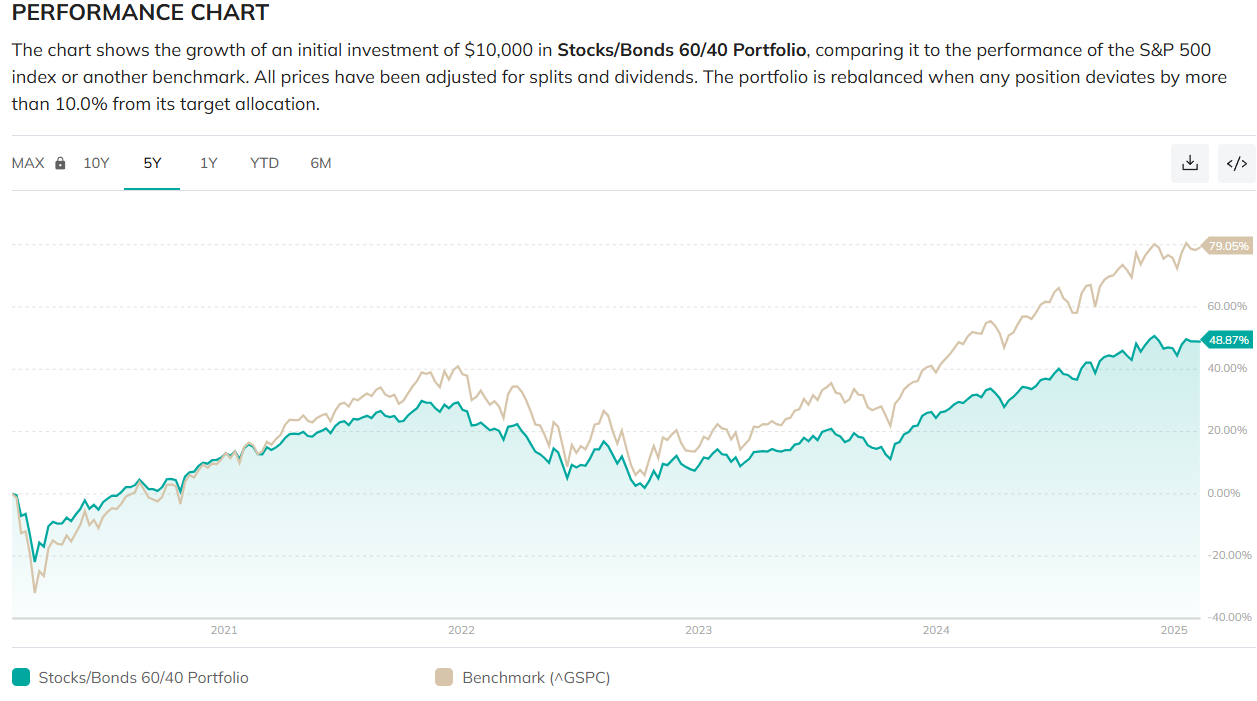

In conclusion, managing risk in the stock market for 2025 requires a proactive, informed approach. While the 60/40 portfolio is the “old faithful” of strategy, it might need tweaking to adapt to the new economic realities of today if we want to extract the most value possible for the least amount of risk. Diversifying more broadly can prepare your investments for various economic scenarios, including the one we face today at the outset of 2025. Ultimately, the key to managing risk is not just about avoiding losses but also about positioning your portfolio to capitalize on opportunities, ensuring your investments are as resilient and adaptive as possible in the face of market uncertainties. With all of what has been said, it may come as no surprise to you that I strongly advocate for using up to 20% of a person’s portfolio for making well-researched, fact-based, stock trades with pre-determined entry prices and exit plans on companies that if the trade didn’t work out we wouldn’t mind holding for the longer term. In my experience, an actively managed portfolio 80% dedicated to low-risk investments and 20% dedicated to more risky investments with a potential for a great payoff will net an investor the greatest returns over 10 years. The below comparison shows 3 separate 60/40 ETFs compared with 3 separate equities ETFs over the past 5 years.