Why Kaspi Stock Could Be the Next Big Fintech Win (NYSE: KSPI)

How a emerging market electronics store became an economic powerhouse, breaking down what the value is of Kaspi stock.

Kaspi.kz, Kazakhstan’s fintech giant, powers its super app with booming digital payments and e-commerce growth. At a $20B valuation, is Kaspi stock undervalued? Its 2024 financial performance—$5.3B revenue (up 28% YOY), 42% margins—suggests yes, especially with dividends at 6% and a Nasdaq listing boosting visibility. But first, let’s look at where they started.

Kaspi, officially known as Kaspi.kz (KSPI), began its journey in Kazakhstan with humble roots that trace back to the entrepreneurial vision of Vyacheslav Kim. In 1993, Kim, a graduate of Almaty State University, founded Planeta Eletroniki, a retailer specializing in household electronics, akin to a Kazakhstani version of Best Buy. Over the next decade, he grew it into the country’s largest electronics retailer, capitalizing on the post-Soviet economic landscape despite challenges like limited consumer credit and liquidity.

By the late 1990s and early 2000s, Kazakhstan’s economic conditions made it tough for retailers to thrive without offering financing options. Many stores, unable to issue loans independently, were acquired by banks. Following this trend, Kim saw an opportunity to address the lack of consumer financing by acquiring a small, recently privatized bank called Kaspiskiy in 2002. Reflecting on this move, Kim later admitted it was partly naive, saying, “All successful entrepreneurs have bought banks, and we are no exception. It’s true, we didn’t know what banking was.” The goal was to integrate banking services with his retail business to facilitate customer purchases through loans, but syncing the two proved challenging.

The turning point came with the involvement of Baring Vostok, a Moscow-based private equity firm founded by American Michael Calvey in 1994. In 2006, Baring Vostok invested in Kaspiskiy, and a year later, in 2007, brought in Mikhail Lomtadze as CEO. Lomtadze, a Georgian Harvard Business School graduate with a background in auditing and consulting, had met Calvey in 2002 and joined Baring Vostok before jumping ship to lead Kaspi. His arrival marked a radical shift. Facing the 2008 global financial crisis, which squeezed both the bank’s profitability and electronics demand, Lomtadze orchestrated a bold pivot. He overhauled the management team, famously stating they “basically fired everybody” to rebuild with young, tech-savvy talent, shunning traditional bankers. The bank rebranded to “Kaspi Bank” (later Kaspi.kz), shifting focus from commercial lending to consumer-centric innovation.

Under Lomtadze’s leadership, Kaspi transformed into a technology-driven company. In 2012, it launched a payments business, followed by an e-commerce marketplace in 2014, and a mobile app in 2017 that evolved into a “Super App.” This app integrated services like bill payments (initially free, disrupting the fee-based norm), lending, shopping, and more, leveraging data and technology for speed and accessibility. Kim and Lomtadze’s partnership deepened, with Kim transferring significant shares to Lomtadze over the years—formalized in 2018 after a decade of informal trust—making them the largest individual shareholders alongside Baring Vostok.

By 2020, Kaspi.kz had grown into Kazakhstan’s leading fintech and e-commerce ecosystem, serving millions with its seamless digital platform. That fall, it went public on the London Stock Exchange, becoming the country’s most valuable public company. In January 2024, it raised $1 billion via a Nasdaq IPO, further cementing its global presence before delisting from London in March 2024 to focus on trading there. What started as an electronics store morphed into a $20 billion-plus super-app empire, driven by a retailer’s ambition, a banker’s reinvention, and a relentless push for innovation in a frontier market.

So, that’s a lot of information… But what we as investors really care about are the numbers, not the heartwarming story of the Amazon of the East. Let’s look at the numbers.

Business Model: The Kaspi Super App Ecosystem

Kaspi operates a two-sided platform:

Kaspi.kz Super App (Consumers): This is the main app for everyday people. You can pay bills, shop online, get loans, manage government services (like renewing a driver’s license), and even transfer money to friends—all in one place. It’s like having your wallet, store, and bank teller in your pocket.

Kaspi Pay Super App (Merchants): This is for businesses. Shop owners use it to accept payments, list products for sale, and access financing. It’s a one-stop shop for small businesses to connect with customers.

The ecosystem has three key pillars:

Payments: Handles billions in transactions—think of it as Kazakhstan’s Venmo or Apple Pay, but bigger locally. It’s the largest driver of the cash-to-digital shift in the country.

Marketplace: An online shopping platform like eBay or Amazon, connecting buyers and sellers without Kaspi owning inventory (keeping costs low).

Fintech: Offers loans, deposits, and financial tools. Kaspi is Kazakhstan’s top lender for consumer loans, beating traditional banks.

This all-in-one approach creates a “flywheel”: more users attract more merchants, which brings more users, and so on. Over 12 million Kazakhs (out of 19 million total population) use the app monthly, with 60% logging in daily.

Kaspi’s Financial Performance: By the Numbers

Kaspi.kz financial performance shined in 2024, showing why it’s caught investors’ eyes. Here’s a snapshot based on its latest reported data (up to mid-2024):

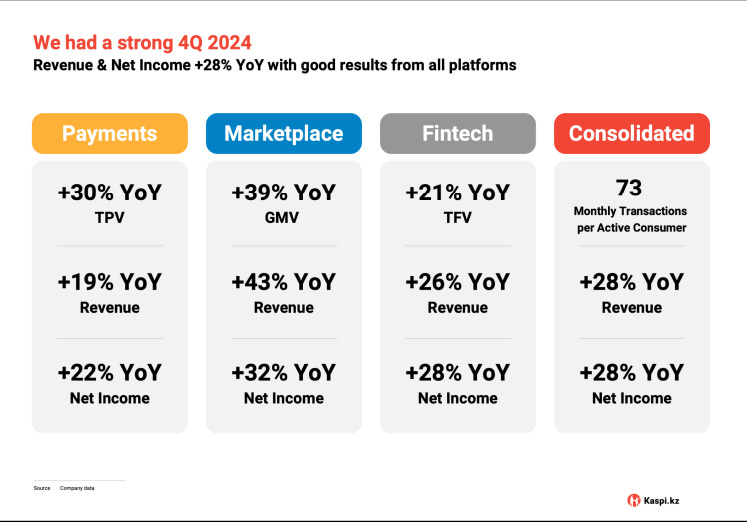

Revenue Growth: In 2024, revenue hit $5.1 billion, up 28% from 2023. For the first half of 2024, it’s tracking even higher. Payments and fintech drive most of this, with marketplace growing fastest for a second year in a row at 39%.

Profitability: Net income in 2024 was $2.1 billion, with a profit margin near 45%. That’s huge—most tech companies dream of margins this high.

Transaction Volume: The app processed $166 billion in payments and marketplace sales in 2024, seven times what it did in 2019. In FY 2024, Payments Platorm had 737,000 merchants and 13.6 million consumers.

Efficiency: Operating costs are low—less than 10% of revenue goes to tech, marketing, and admin. Compare that to global tech giants like Amazon, where costs eat up far more.

Kaspi is a value play and pays dividends too, which is a rarity for growth companies. In 2023, it returned $750 million to shareholders, signaling confidence in its cash flow.

Growth Prospects: Where’s It Headed?

Kaspi’s growth story isn’t slowing down. Here’s why:

Kazakhstan Dominance: With 90% of public services digitized via its app (partnered with the government), Kaspi is baked into daily life. E-commerce in Kazakhstan jumped from 1.4% of retail in 2018 to 13% in 2023—Kaspi owns most of that.

Regional Expansion: Kaspi’s eyeing Central Asia and beyond. In 2024, it bid to buy Uzbekistan’s Humo payment system, a state-backed network with 10 million users. Kaspi Uzbekistan expansion could double its revenue alone.

Turkey Acquisition: Kaspi recently acquired Hepsiburada, a e-commerce platform in Turkey with 12 million active consumers. Turkey’s $172 billion retail market is approximately 4x the size of retail spending in Kazakhstan

Innovation: New features like QR payments with China’s Alipay+ (2024) and potential multi-language support could open doors to foreigners and tourists.

Economic Tailwinds: Kazakhstan’s economy is growing (4-5% GDP annually), fueled by oil and a young, tech-savvy population. Turkey’s economy is also growing by more than 4% annually.

But it’s not all a rosy sunshine giggle fest—growth depends on execution and navigating risks (more on that later).

Risks and Challenges

Every company has its kryptonite. Here’s what could trip Kaspi up:

Short-Seller Scrutiny: In September 2024, Culper Research shorted Kaspi, alleging it misled investors about ties to Russia (claiming 30% of revenue comes from there) and past dealings with shady figures. Kaspi denied this, and Kazakhstan’s financial regulator backed them, saying they comply with U.S./EU sanctions. Still, the stock dropped 20%, showing how sentiment can sting.

Russia Exposure: Posts on X speculate Russia could be a growth driver if sanctions lift post-Ukraine war. But if sanctions tighten, any Russian ties (even minor) could invite trouble—think fines or delisting risks.

Market Saturation: Some users on X note Kaspi’s dominance in Kazakhstan might be peaking—loan rates are high (20%+), marketplace fees are up (15%), and cashback perks are fading. Competitors like ForteBank are fighting back.

Geopolitical Risk: Kazakhstan borders Russia and relies on it economically. Political instability or sanctions bleed-over could hurt Kaspi indirectly.

Valuation Debate: At a $20 billion market cap (post-drop), Kaspi trades at 10x earnings—cheap for a tech stock but pricy if growth stalls or risks materialize.

Valuation: Is It a Buy?

Let’s use the very basic Discounted Cash Flow (DCF) idea from this post to think about Kaspi’s worth. Assume:

Future Cash Flows: If profits grow 20% annually for 5 years (a more conservative number given 25% in 2024), then slow to 5%, Kaspi could generate $3 billion net income annually by 2029.

Discount Rate: Use 12% (we will use a higher and more conservative number than the 10% example). Discounting those flows back suggests a value of $25-30 billion today—25-50% above its current $20 billion cap.

Per Share: With 200 million shares, that’s $125-150 per share vs. $100 now (February 24, 2025).

This aligns with some analysts’ views (e.g., NextGen Investors’ 117% upside call in November 2024, JP Morgan's $137/share call in December 2024).

Why Kaspi Stands Out

Kaspi’s not just a bank or app—it’s a lifestyle platform. I personally have missionaries we support in Kazakhstan I have spoken to about Kaspi, they use it for their clinic they run and also use it for their personal use. They love the App! Harvard Business School has also written two case studies on it, "Kaspi.kz: Building Trust through Innovation.", praising its trust-building after a 2014 bank run and its tech pivot. Its 1,200-person tech team (out of 9,000 employees) keeps it ahead, and its asset-light model (no warehouses, just software) pumps out cash. Plus, being Kazakhstan’s first Nasdaq listing gives it a pioneer glow.

Now, Lets get deep into intrinsic value numbers:

Step 1: Simplified DCF for Kaspi.kz

Let’s build a basic DCF to estimate Kaspi’s intrinsic value, then derive a per-share price to compare with its current market price and peers.

Starting Point: 2024 Free Cash Flow (FCF)

Kaspi doesn’t publicly break out FCF quarterly, but we can estimate it from net income and capex. In 2023, FCF was ~$1.7 billion (net income $1.9 billion minus ~$200 million capex). For 2024, net income is $2.1 billion, and capex remains low (asset-light model). Assuming similar capex, FCF is ~$2.05 billion.

Growth Projections

Kaspi guides 20% net income growth for 2025, excluding Türkiye (Hepsiburada acquisition). Let’s assume:Years 1-5 (2025-2029): 20% FCF growth, slowing as Kazakhstan matures.

2025: $2.58 billion

2026: $3.1 billion

2027: $3.72 billion

2028: $4.46 billion

2029: $5.35 billion

Terminal Growth: 3% (conservative, tied to global GDP growth).

Discount Rate

Use 12%—higher than the 10% U.S. norm due to Kazakhstan’s emerging market risk (e.g., currency volatility, geopolitical exposure). This reflects a Weighted Average Cost of Capital (WACC) factoring in Kaspi’s low debt and equity risk premium.

Discounting Cash Flows

Discount each year’s FCF back to today (February 24, 2025):2025: $2.58B / 1.12 = $2.3B

2026: $3.1B / (1.12²) = $2.47B

2027: $3.72B / (1.12³) = $2.64B

2028: $4.46B / (1.12⁴) = $2.83B

2029: $5.35B / (1.12⁵) = $3.03B

Total 5-year discounted FCF = $13.27B.

Terminal Value

At year 5 (2029), FCF = $5.35B. Terminal value = $5.35B × (1 + 3%) / (12% - 3%) = $61.24B. Discounted back: $61.24B / (1.12⁵) = $34.73B.

Total Value

Enterprise Value = $13.27B (5-year FCF) + $34.73B (terminal) = $48B. Add $1.2B cash (9M 2024), subtract negligible debt: Equity Value ~$49.2B. With 200 million shares, that’s $246/share—over twice the current $100/share ($20B market cap).

Step 2: Peer Comparison Setup

Kaspi’s $20B market cap and 8.5x P/E (2024 earnings) look cheap next to peers, but the DCF suggests significant upside. Let’s compare with fintech/e-commerce players based on P/E, growth, and implied DCF multiples. I’ll use 2024 data where available, projecting 2025 roughly.

Peers:

PayPal (PYPL)

Market Cap: $82B

2024 Net Income: ~$4.5B (up 10% YoY)

P/E: 18x

Growth: 8-10% revenue, slower than Kaspi’s 32%.

Implied DCF: Trades at 2-3x FCF (mid-20s), reflecting mature U.S. market.

Block (SQ)

Market Cap: $53B

2024 Net Income: ~$1.2B (up 50% YoY, uneven profitability)

P/E: 44x

Growth: 15-20% revenue, Cash App focus.

Implied DCF: ~30x FCF, high due to growth bets (e.g., Bitcoin).

MercadoLibre (MELI)

Market Cap: $103B

2024 Net Income: ~$1.8B (up 30% YoY)

P/E: 57x

Growth: 35% revenue, Latin America leader.

Implied DCF: 40x FCF, premium for emerging market growth.

Sea Limited (SE)

Market Cap: $57B

2024 Net Income: ~$0.5B (first profitable year)

P/E: 114x

Growth: 20-25% revenue (Shopee, Garena), SEA focus.

Implied DCF: 50x FCF, volatile profitability.

Step 3: DCF vs. Peers

Kaspi’s DCF Multiple: $49.2B valuation ÷ $2.15B 2024 FCF = 23x FCF. Current market price ($20B) is 9x FCF—way below peers.

P/E Comparison:

Kaspi: 8.5x (2024), 7x (2025 at $2.82B net income, 20% growth).

PayPal: 18x—double Kaspi’s, despite slower growth.

Block: 44x—over 5x Kaspi’s, less consistent profits.

MercadoLibre: 57x—7x Kaspi’s, similar growth but pricier market.

Sea: 114x—13x Kaspi’s, high risk/reward.

Growth-Adjusted P/E (PEG):

Kaspi: 8.5 ÷ 25 = 0.34 (2024 growth).

PayPal: 18 ÷ 10 = 1.8.

MercadoLibre: 57 ÷ 30 = 1.9.

Kaspi’s PEG is dirt cheap—growth isn’t priced in.

DCF Implied Upside:

Kaspi’s $246/share DCF suggests 146% upside from $100.

Peers’ DCF multiples (20-50x FCF) imply Kaspi could trade at $43B-$107B (21x-50x $2.15B FCF), or $215-$535/share, if aligned with their growth premiums.

Step 4: Why the Gap?

Kaspi’s DCF ($49.2B) far exceeds its $20B market cap, while peers trade closer to their implied DCF values. Reasons:

Market Perception: Kazakhstan’s frontier status spooks investors—geopolitical risk (Russian war) and short-seller noise (Culper’s 2024 report) cap enthusiasm.

Liquidity: Nasdaq listing is new (2024); lower U.S. trading volume vs. peers.

Dividend Drag: Kaspi’s 6% yield (62% payout) signals maturity, not pure growth, unlike MercadoLibre or Sea.

Peers like MercadoLibre (Argentina-based) overcame similar doubts as growth proved out, suggesting Kaspi’s discount could narrow if execution holds.

Conclusion

Kaspi’s DCF ($246/share) screams undervaluation at $100/share (8.5x P/E), especially versus peers like MercadoLibre (57x) or even PayPal (18x). Its 25% growth and 42% margins outshine most, yet it trades at a fraction of their multiples. If Kaspi matched MercadoLibre’s 40x FCF (reasonable given similar growth), it’d be $86B ($430/share)—still below Sea’s speculative 50x. The catch? Investors aren’t fully buying the story—yet. Expansion success (e.g., Hepsiburada) could bridge the gap.

Citation

Sucher, Sandra J., Fares Khrais, and Marilyn Morgan Westner. "Kaspi.kz: Building Trust through Innovation." Harvard Business School Case 324-022, September 2023. (Revised June 2024.)

The Kazakhstan bond yield is 14%, so you can't use a 12% discount rate. I suggest 20% in which case the stock isn't cheap

Interesting find, note that the Turkey market is very competitive and Alibaba (Trendyol) is a big player there. Just a small note.